SIMILAR SIGNALS HAVE BEEN COMING from the Global Dairy Trade (GDT) based in the world’s largest dairy product export country, New Zealand. GDT posted its sixth positive biweekly trading session since December 4. At the last event, six of the seven dairy products sold higher.

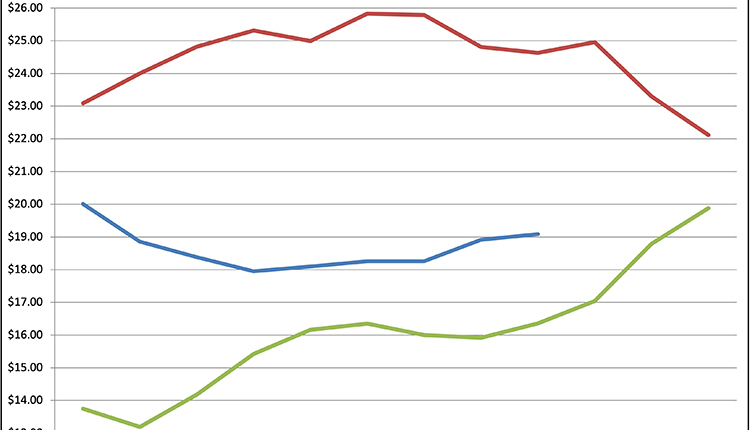

USDA PROJECTIONS MIRROR current market signals. The federal agency’s economists raised the All-Milk midpoint price projection from $16.80 to $17.25 for 2019, up 45 cents per cwt. during the past 60 days. The anticipated range would fall between $16.90 and $17.60.

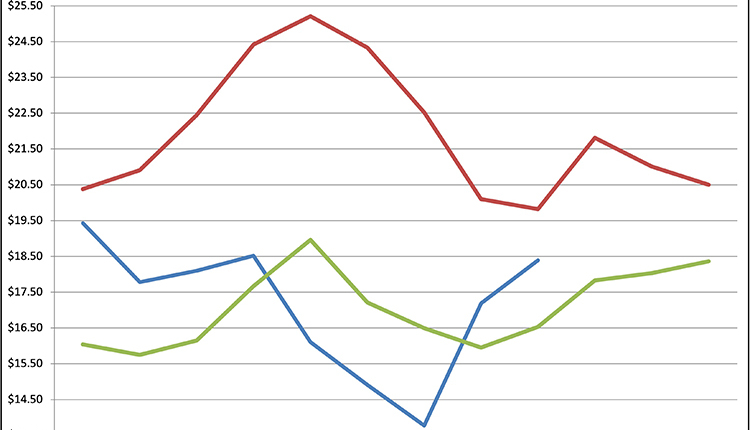

DESPITE AN IMPROVED FORECAST, paultry margins still existed on the farm with a December 2018 Milk-Feed ratio at 2.04. The USDA calculation was based on $16.40 per cwt. milk sales, $3.54 per bushel corn, $180 per ton alfalfa hay, and $8.57 per bushel soybean costs.

NEGATIVE RETURNS CAUSED dairy farmers to step up culling throughout 2018 as 3.15 million dairy cows were sent to slaughter through late December. That was up 157,800 head over the previous year.

THAT CULLING INCLUDED REPLACEMENTS as prices tumbled to a $1,140 per head average, with a range from Virginia’s $970 to Oregon’s $1,350. These values were $100 per head under the 2009 low of $1,240.

A PLANNING PRICE OF $15.80 per cwt. was established by the USDA’s Farm Service Agency for January to March loans. In the previous quarter, that value had been $16.10 and $15.20 the same time last year.

DECEMBER MILK SLOWED to a 0.5 percent growth rate nationally, as 11 of the 23 major milk states produced less milk. Colorado led all gainers, up 6 percent. California climbed 1.7 percent, Wisconsin 1.4.

U.S. MILK FLOW EXPANDED 0.9 PERCENT to reach 217.5 billion pounds for the 2018 calendar year, suggested preliminary USDA estimates. Milk cows totaled 9.39 million head and averaged 23,173 pounds each.

WHOLE MILK AND FLAVORED WHOLE MILK buoyed fluid milk sales by accounting for 15 billion and 747 million pounds, respectively. Those totals were up 1.6 and 12.6 percent for the year. Whole milk now accounts for 32 percent of the market. All other fluid categories were down.

BRIEFLY: Hauling costs climbed 7 cents to reach a 28-cent average in the Upper Midwest Federal Milk Marketing Order. Costs ranged from 75 cents per cwt. for the smallest producers to 16 cents for the largest group. Dairy product imports into the U.S. fell 4.6 percent in 2018. Meat inventory reached a record of 2.6 billion pounds, placing downward pressure on prices. The situation could persist throughout 2019.

In your next issue . . .

PASTEURIZATION SAVES LIVES.

When foodborne illness outbreaks occur, whole-genome sequencing can pinpoint the exact source, as has been the case with infections caused by unpasteurized milk.

HEAT STRESS LINGERS FOR GENERATIONS.

The effects of dry period heat stress span three generations and are likely tied to epigenetics.

THE RIGHT ALFALFA-GRASS MIX.

New alfalfa and grass varieties create opportunities for successful mixtures that can improve yield and milk production.