More U.S. dairy products have likely moved through government programs in 2020 than at any other point in the past 30 years. How much of an impact have those purchases had on dairy prices?

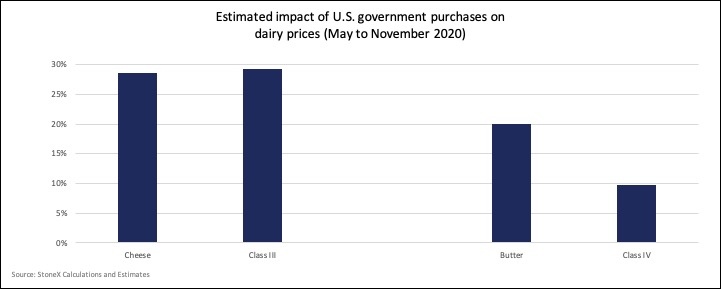

My best guess is that the government purchases likely added 64 cents per pound (+28.6%) to the CME block price from May through November. As for butter, government purchases added 31 cents (+20.1%).

That means the purchases pushed the average Class III price about $6.30 per hundredweight (cwt.) higher than it otherwise would have been, and Class IV was about $1.31 per cwt. higher. While there is room to debate my estimates and methodology, there is no doubt the government purchases have had a big impact on market prices.

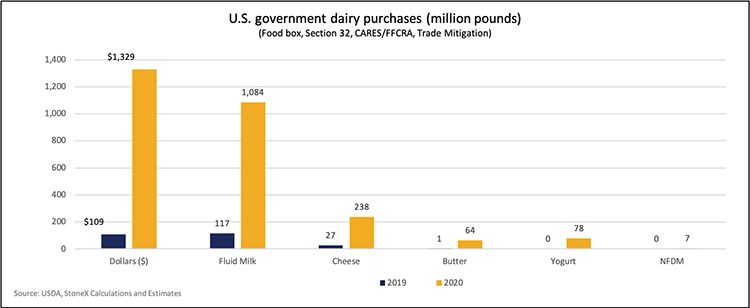

The USDA has been making purchases with money allocated from a numbers of sources. We can track the specific cost and volume of dairy products purchased with Section 32, CARES/FFCRA, and Trade Mitigation funds, but the USDA has not released details on exactly what was included in the food boxes delivered during 2020. The lack of food box detail is disappointing.

From my calculations, about $1.1 billion has been spent on purchasing dairy products through the food box program this year compared to only $214 million across all the other programs. By my estimates, the USDA has spent $1.33 billion, purchasing 1.1 billion pounds of bottled milk (128 million gallons), 238 million pounds of cheese, 64 million pounds of butter, and 78 million pounds of yogurt. All of those numbers are up 800% or more from 2019.

Translating the government purchases into price impact requires some assumptions, a mild suspension of disbelief, and a little witchcraft. The first issue to deal with is retail cannibalization. All, or nearly all, of the dairy products purchased through these government programs were given to food banks or distributed directly to people in need. If these consumers were not given free dairy products, they likely would have purchased more dairy through retail or food service.

In my estimates, I’m assuming 20% cannibalization, meaning every pound of free product distributed reduces retail sales by 0.20 pounds (20%). The real number could be higher or lower. Since the government hasn’t handed out free dairy products on this scale in decades, we don’t have any recent statistical studies on cannibalization rates.

A challenging calculation

The next issue to deal with is the dynamics within the dairy markets. If the government stepped in and bought a bunch of product for a month or two and caused a single large shock, assessing the impact would be easier. But there have been multiple shocks as new rounds of the food box program were announced and the purchases have been spread over a seven month period. I’ve kept this analysis very simple. I’m calculating how much of each product the government likely purchased each month, subtracting the cannibalization, and then adding the purchased product back to inventory.

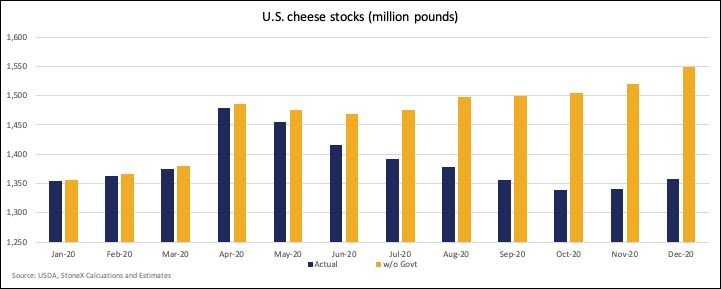

Actual cheese stocks at the end of October were 3 million pounds lower than last year, but without the government purchases stocks could have been 163 million pounds higher than last year, although that probably overstates the inventory level. Without the government purchases, milk prices would have been weaker, milk production would have been lower, and cheese production, theoretically, would have been lower and inventories would not have built up as much.

With weaker prices, exports would have been stronger and imports would have been weaker, too. A more dynamic model may find less of an impact from the government purchases if it can take into account the shifts within the dairy supply and demand system.

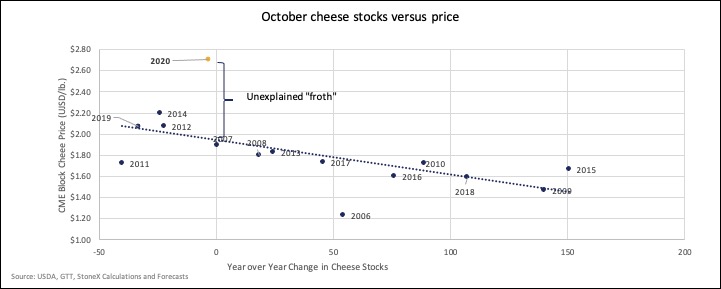

The next step is translating the higher estimated stocks into a price impact. The issue is, cheese prices have disconnected from the typical fundamentals. It is true that the large government purchases have kept cheese stocks from growing, but the level of cheese stocks that we had in October would suggest a CME block cheese price of $1.88 per pound. Instead, the market averaged a record high $2.71, which was 83 cents higher than what you can justify given the amount of cheese sitting in inventory.

So, what do you ascribe that extra 83 cents to?

Retailers stocking up for the holidays?

Restaurants running on lean inventory and suddenly needing some product?

Buyers getting concerned about availability and overpaying just to assure themselves of some supply?

Or do you attribute it to the very large government purchases spiking the market above and beyond the fundamentally justified level?

I’m assuming that 70% of the overpricing on cheese since May is due to the government purchases and 30% is due to the other factors in the market. The real breakdown could be different, but this is my best guess.

So, how much of an impact have government purchases had on prices this year?

We’re unsure about how much volume the government actually bought. We’re unsure about how much retail/foodservice cannibalization it created. We’re unsure about how bad the fundamentals would have been without the government purchases. And lastly, we’re unsure about how much of the froth in the cheese price is due to government purchases versus other factors. I’ve made my best effort to account for these things, but future estimates may show a larger or smaller impact than what I’m currently estimating. What we do know is that the purchases have had a big impact for dairy prices this year, particularly for cheese.