Sorry, in a click bait world I feel like I have to open with a title that grabs a reader’s attention.

However, the statement is true.

The cost of nearly everything has gone up for dairy farmers and farm level margins are being squeezed. What markets do care about is how much supply is available, and there is better news for farmers there.

Due to the tighter margin, the milk supply has tightened significantly during the second half of 2021, and it looks like it is going to stay weak for the first half of 2022. That has pushed dairy prices higher.

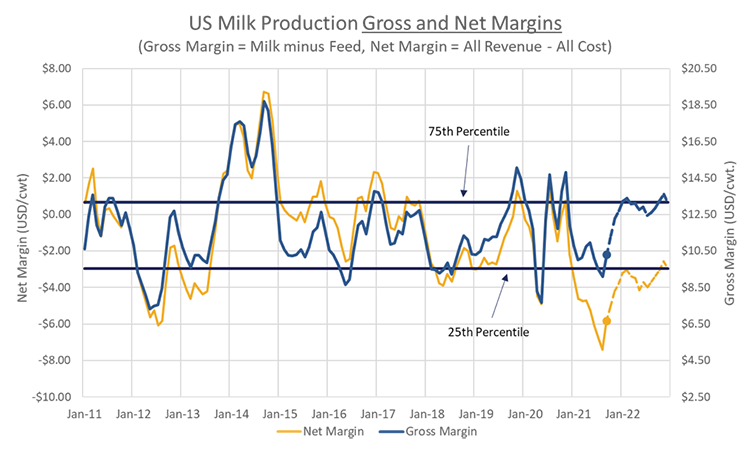

As a dairy market analyst for the past 16 years my main gauge of farm profitability has been my gross margin calculation, which is the price of milk minus the price of feed. You can generally assume the other costs are steady or slowly climbing with increases for some items likely offset by declines in prices for other products in any particular year.

From a long-term perspective, gains in farm level efficiencies generally offset the small year-to-year uphill movement in those other costs. The gross margin has worked well as both a long and short-term profitability indicator. But with input prices increasing sharply this year, the gross margin may not be giving a full picture of farm level financial stress.

The USDA attempts to estimate total costs of milk production and calculates a net margin at an annual level for farms of different sizes. I’ve tried to take those annual costs and convert them into monthly costs by tying the various input costs for a dairy farm with 500 to 999 cows to monthly indices like the cost of energy for dairy farms tied to the price West Texas crude oil. When I couldn’t find a good monthly price to tie the cost to, I assumed it was up 4%, which was the year-over-year change in the core Consumer Price Index (CPI) during September and October. From 2011 to 2020 the gross margin and net margin calculation track each other closely. But with my estimated cost movements for 2021, the net margin has dropped to some very financially painful levels.

The gross margin fell this year and bottomed out near the 25th percentile of the 10-year range. That would suggest mild financial pressure for dairy farms and a small drop in the size of the herd. But the U.S. dairy cow herd has dropped 107,000 cows (-1.1%) between May and October.

That isn’t a record reduction, but it is the largest since 2009 and it does not correlate with the relatively minor drop in the gross margin. But if you look at the net margin estimate, it has dropped to its lowest level since 2009, and suddenly the decline in the national herd and big slowdown in milk production this year makes more sense than when I was just looking at the gross margin.

With feed costs pulling back from where they were early in the year, and the lower milk production helping to push milk prices higher, the margin outlook improves for the remainder of this year and into 2022. If you look at the gross margin, it rebounds to the 75th percentile, which would suggest margins are going to be well above average and should encourage a rebound in milk production. But the net margin only rebounds to the 25th percentile, which would be well below average margins for 2022.

For now, I think we have to put more weight on the net margin calculation, which means financial stress at the farm level may be with us for a while and milk production growth will remain weak in 2022. Maybe that will help to push milk prices, and hopefully margins, higher than I’m currently forecasting.